Targa Resources ($TRGP) - A reversion to its aggressive growth roots

Targa Resources ($TRGP) - A reversion to its aggressive growth roots

So far, so good!

Targa’s aggressive pivot towards becoming the top dawg in the Permian gas and NGL space has finally been paying off. Years of debt raises, equity issuances, and asset divestitures got them to where they are today, putting them in a prime position to capture the advantage of higher spreads at Waha in the near-term and increasing Gulf Coast NGL + natural gas demand in the long term.

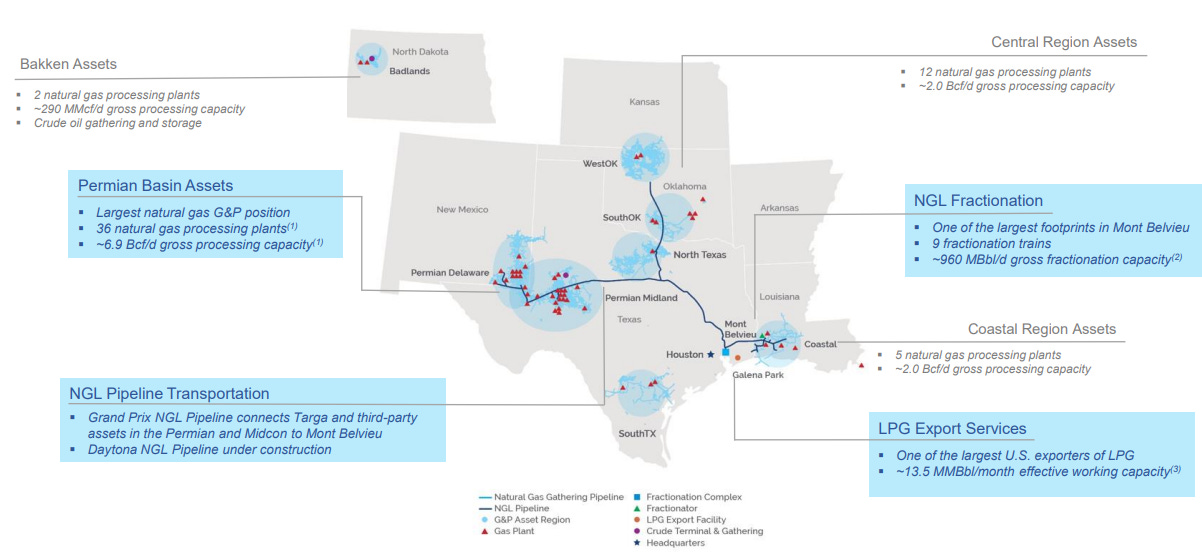

Not only do they dominate in the Permian, but their robust interconnectivity with the Gulf Coast, fractionation footprint and LPG export presence allows them to control the molecule from wellhead to international consumer. Fewer molecules exchanging hands = lower costs = higher margins.

In this post we dive into Targa Resources ( TRGP 0.00%↑ ), a $17 billion natural gas and NGL midstream corporation. It’s unique in that it carries a vastly different risk profile than the other North American gas infrastructure behemoths.

For the sake of “getting to the point,” we will save the (interesting) story of TRGP’s historic aggressive growth strategy to cement itself as a leader force to be reckoned with for a later date.

We’ll first go through their capital allocation profile, where the strategy is shifting, a look at some organic growth projects, and tie it all into an informed outlook on the stock’s future return profile.

We won’t go through industry-specific drivers, as they’ve been laid out in prior posts discussing the case for natural gas infrastructure in the Permian. The three primary drivers being:

These drivers underpin our investment case for all the quality Permian gas infrastructure companies. Though it’s worth looking at them individually to assess where risk-reward seems to be mispriced.

Proper Capital Allocation Drives Outsized Returns

The first thing I do when analyzing infrastructure companies is look at their cash flow profile, how its been trending, and where it’s likely headed. This is absolutely crucial for the potential success of companies like Targa. We want to know how they’re allocating their cash from operations.

It gives us a look at whether its been going towards debt reduction, capex, or shareholders in the form of buybacks or dividends. These capital allocation decisions WILL make or break a stock.

One misstep and the stock gets clobbered by investors with no remorse.

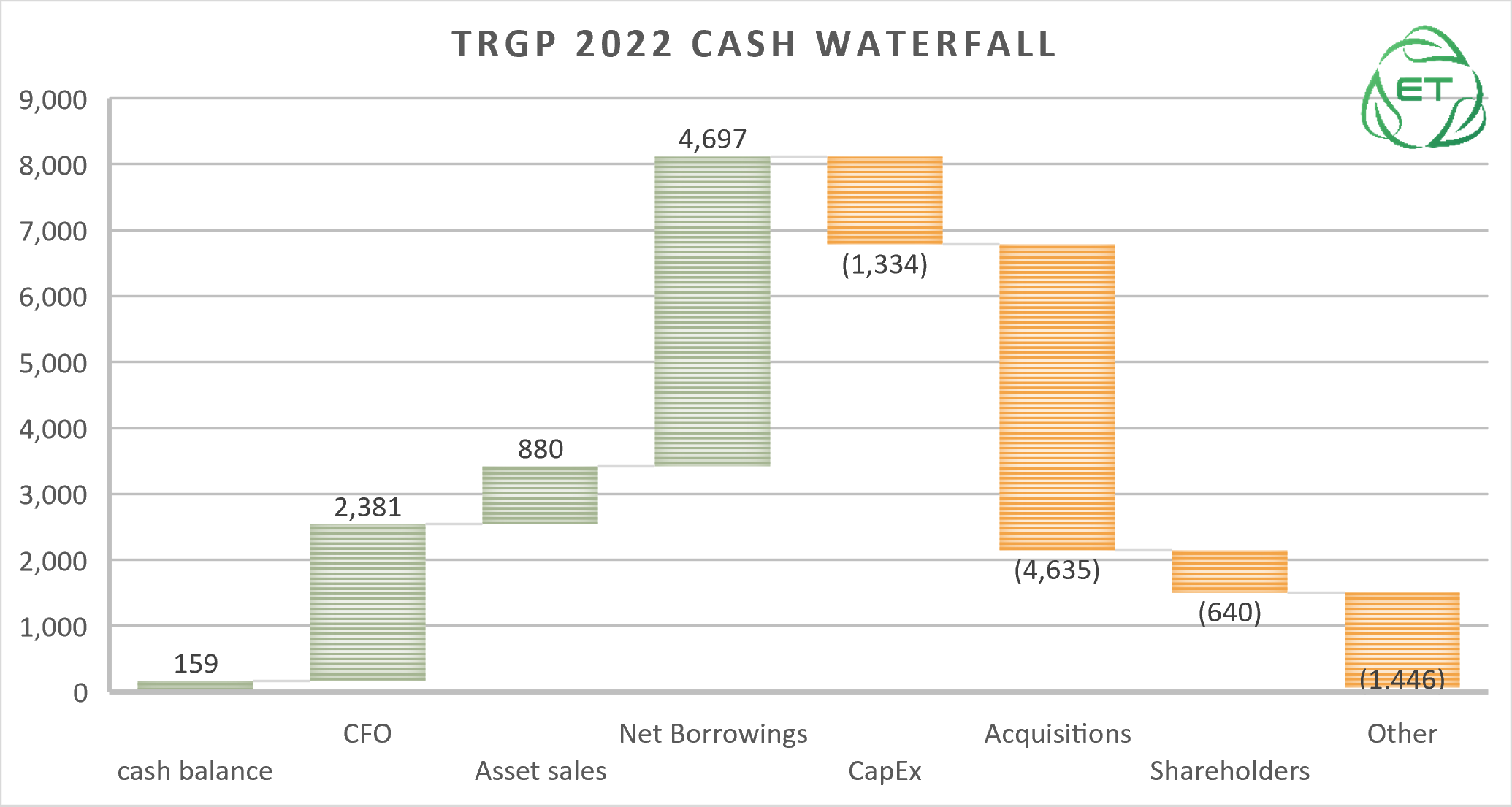

Lets look at Targa’s sources and uses of cash in 2022:

2022 was a bit messy. Mainly driven by the $3.6 billion acquisition of Lucid Energy, which substantially increased its exposure to Delaware processing capacity.

The chart tells the whole story. $2.4 billion of cash from operations was not enough to fund the total $5.9 billion of acquisitions + capex during the year. So Targa tapped the debt markets and its revolving facilities for $4.7 billion to fund these outlays.

This looks vastly different from 2021, when Targa reduced capital spending and used the majority of its cash from operations to de-lever its balance sheet.

On top of its industry-leading 90% dividend cut in the wake of COVID, it was this prudent strategy that led the stock to 11x its value from 2020 lows.

Following the growth strategy in 2022, though the stock has risen a comfortable 40%+, investors should wonder what capital allocation strategy management will likely pursue, as it will impact investors appetite for the stock.

Will the company continue to lever up and acquire assets, or focus on executing its current project backlog to return cash back to shareholders? Let’s find out.

Squaring Targa’s Capital Allocation Strategy with the Strength of its Portfolio

The two key question we need answered to determine whether TRGP is a stock we should invest in today:

Does management look to repeat its 2022 growth strategy in 2023+?

If so, will the industry environment be conducive to the growth of the acquired assets + its organic portfolio?

Management’s Guidance

Though should be taken with a grain of salt, it’s important to understand what management is communicating to its shareholders in terms of future capital allocation. Let’s see what kind of language they’ve used to prepare investors for what’s to expect re: Capital Allocation Strategy:

“on capital allocation, our priority within how we want to spend both organically and return capital to shareholders. We want to start with a strong balance sheet and make sure we have flexibility to continue to invest and to continue to return capital to shareholders over time.”

Matt Meloy, CEO

Not entirely helpful.

So reduce debt, continue to invest, and return capital to shareholders.

They always try to thread the needle when answering questions like this in order to verbally hedge all their bets. Seeing this enough times, we’re still able to read between the tea leaves which says: growth is likely in their future. Because otherwise, they would have de-emphasized the “continue to invest” portion of the capital allocation response. Or clarify that they will just execute the projects in their organic backlog.

We have a sense of what capex spend will look like given this backlog, but further debt-raises for acquisitions or further project build-outs is a risk, in our opinion, as it delays shareholder returns even further.

Though Targa will still continue to increase shareholder payouts, large % increases will come from a low base level, so returns will ultimately remain relatively low vs. peers due to higher allocations towards de-leveraging and asset growth.

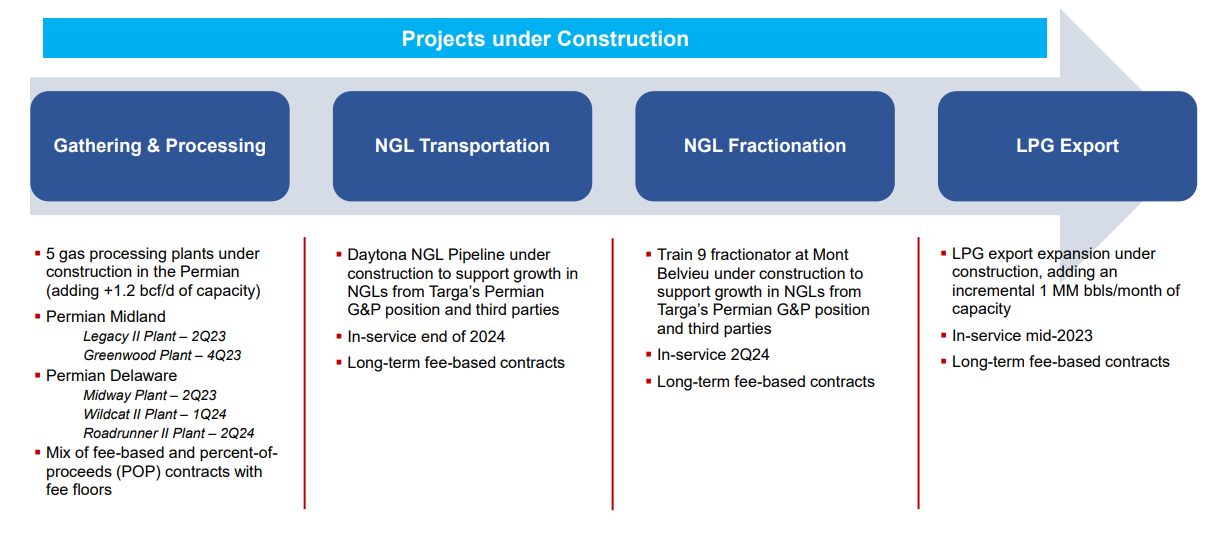

Increasing CapEx

Targa looks to increase capex by nearly 40% in 2023. We’d rather see it being returned to shareholders. But lets see what they look to spend it on.

2 Midland and 3 Delaware processing plants

We went through the rising issue of increasing Gas-to-Oil ratios in the Permian in detail before.

Given Targa’s near-monopoly on Permian processing capacity, they’re one of the few capable of offering reasonable fees to its growing list of credit-worthy customers.

Our opinion: this is a solid capital allocation decision that will make up the bulk of its spending this year.

On top of acquisitions, the increase in EBITDA from these assets entering service in 2023-24 will offset the higher debt it obtained in 2022, subsequently reducing leverage (a function of rising denominator, net debt/EBITDA)

Daytona NGL pipeline

Targa looks to internally secure NGL offtake from those processing plants rather than relying on third parties with less experience and connectivity in the region.

The pipe will connect volumes from these processing plants to its massive Grand Prix NGL pipeline, which will ship volumes down to the Gulf Coast

NGL fractionation

To support the coming influx of NGLs, Targa will construct their 9th fractionation plant at Mt. Belvieu

LPG Export expansion

Greater output from its fractionation facility suggests an increase in export capacity is crucial to tying off its vertical integration strategy, from processing to transportation to fractionation to delivering product to international markets

The Case for Targa Resources

Targa remains committed to its vertical integration strategy – owning the molecules from the Permian and connecting it to buyers in international markets. It solidified its presence in the Permian, is increasing its influence on the Gulf Coast, and following several buyouts of non-controlling interest they’ve become 100% in control of their destiny, riding a rising tide.

Increasing EBITDA generation from acquisitions and projects in its backlog should lead to lower leverage and eventually enable debt paydowns once build-outs are complete. The spending spree appears to be calculated (though not gentle by any means) and in-line with our views on the overall trend of natural gas and NGL markets in the Permian and Gulf Coast

Rising shareholder payouts during a time of investment AND de-leveraging are a good sign of management’s outlook for the stability of its business.

A dividend cut is the LAST thing investors want in a stable infrastructure investment. Many invest in these companies as a long-term source of rising, stable dividend payments.

Risks to the outlook

Targa seems to be making the right decisions to capitalize on the changing dynamics of the Permian and global gas markets in general. One major risk to the outlook, believe it or not, is crude prices.

Though Targa is hardly exposed directly to crude volumes, it’s heavily exposed to gas and NGL volumes in the Permian. Should crude-focused producers in the basin decide to meaningfully ease up on production, it would negatively impact Targa more than it would other gas and NGL infrastructure companies exposed to the Permian.

This is due to their continued growth strategy that resulted in greater debt loads, and excess cash generation won’t materialize into significant shareholder payouts until some de-leveraging occurs. So substantial shareholder payouts are unlikely until at least 2024. A reduction in crude prices would certainly push the timeline back.

Should I invest in this?

Given its current dividend yield of ~2.0%, expected to rise to just 2.5% in 2023, meager buybacks, excess cash to be allocated to debt reduction/growth, and an elevated 2022 multiple of 9.5x (especially vs. its peers), the investment case for TRGP is whether the rising tide of increasing gas and NGL volumes out of the Permian will continue to materialize.

Crude prices will determine this.

High utilizations for its new infrastructure entering service in 2023-24 is crucial for further gains in the stock and higher shareholder returns in the 2024-25 period.

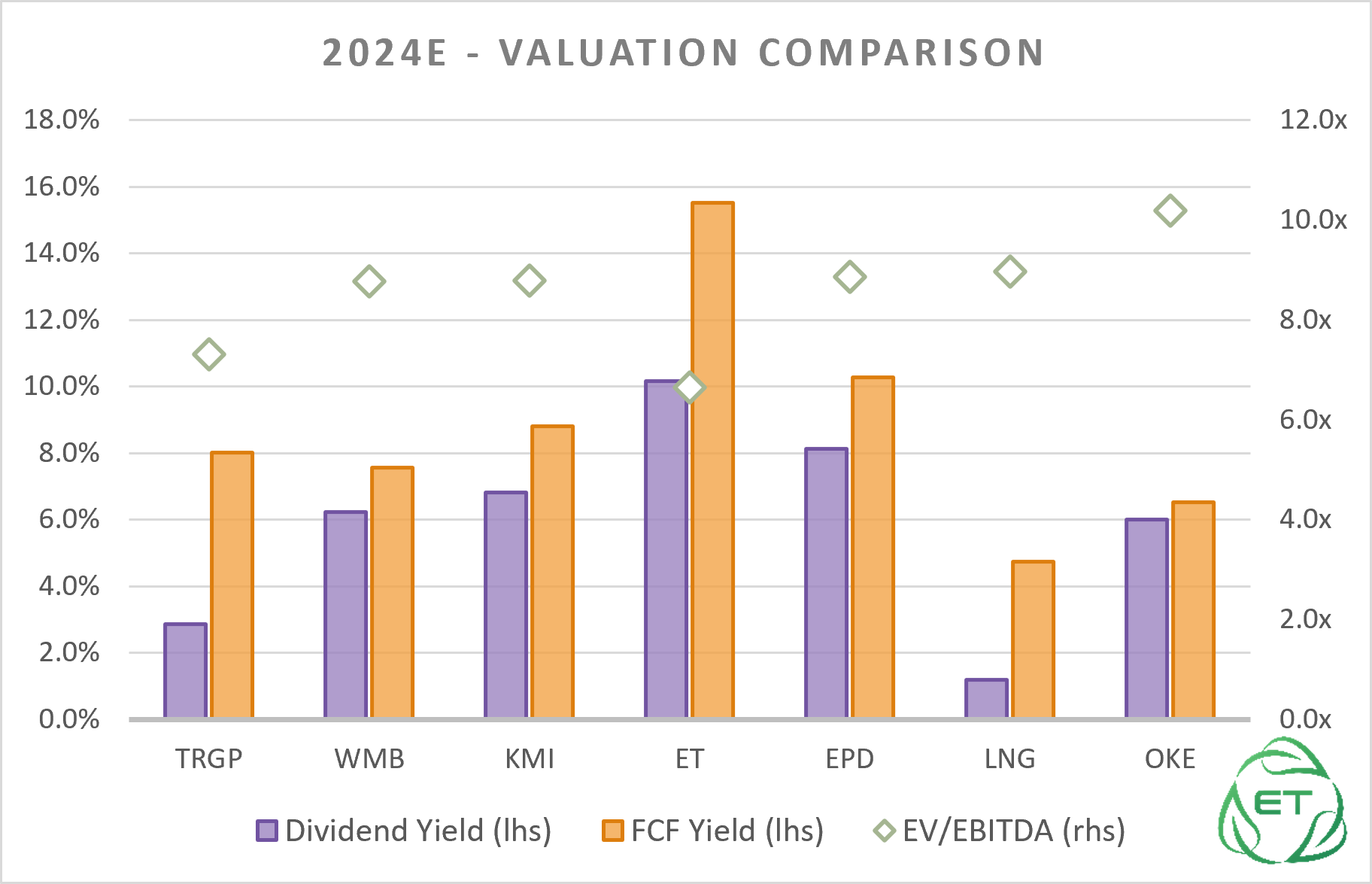

Though the stock looks relatively expensive on a 2022 basis, we should look at 2024e given its bottom line will have materialized its growth pursuits by then. Based on 2024e valuations, the stock looks more attractive compared to its peers on an FCF yield and EV/EBITDA basis (aside from dividend yield).

This favorable 2024e valuation vs. peers (7.3x vs 8.7x) tells us that the market is currently pricing in substantial risk to Targa’s EBITDA targets. This is a fair assessment given the highly uncertain current macro environment.

We think the name is primarily a risk-on play compared to its peers given Targa’s decision to double-down on the rising tide of increasing gas and NGL volumes by building out its vertically integrated business model through higher leverage.

A retreat to $50/bbl crude would lead to an outsized pull-back for TRGP compared to its peers as EBITDA generation falters, reducing its capital allocation flexibility, and risks being downgraded by credit agencies.

Our Take

The valuation is a bit rich at the moment for the amount of earnings (and management) risk the stock carries. For an infrastructure company in this period of elevated macro-economic uncertainty, we would prefer to see higher shareholder payouts in the form of buybacks or dividends.

We have no doubt, however, that the company is in a prime position to capitalize on the trends mentioned earlier and in prior posts, but think a pullback from these levels are likely.

Though we’d strongly consider scaling in once weak investors bail on the long-term outlook, which may occur in 2H23, a more prudent long-term buy and hold strategy would also play in the favor of investors as macro drivers crystallize into Targa’s bottom line around the same time it places its favorable assets in service.

Though we’d forgo juicy dividends by investing in TRGP vs. its higher dividend-paying peers, our confidence in the industry outlook leads us to believe that the stock has substantial more upside than those peers.

TLDR: Sidelines until a pullback, likely 2H23, unless a more prudent strategy is preferred. Scale in to capture the company’s levered upside as bullish Permian and global gas market trends are unlikely to substantially subside. Lower crude prices wouldn’t invalidate the thesis, but will certainly lead to a reduced upside opportunity.

We currently do not own shares in the stock, but look to establish initial exposure on sizable pull-backs. We remain invested in other Permian gas infrastructure names in the meantime.

Tell us what you think

Want to see more fundamental analysis? Elaborate on historic valuation and comparisons? More company history? Model inclusion? More pretty charts? Let us know in the comments!

Disclaimer: None of this is deemed to be financial advice. Don’t risk more than you’re willing to lose. Invest responsibly and with personal conviction.