The Fundamental Case: Coal-to-Gas Switching

Gas Infrastructure Opportunities in the Permian

We continue our Gas Infrastructure Series today and take a look at one of the three key fundamentals driving profitability growth for energy producing and infrastructure companies.

Focus will be on the latter with exposure to Permian. We’ll use this framework to underpin our bull case for gas infrastructure stocks in the long-term.

For the sake of keeping these posts less than 2,000 words, we’ll break The Fundamental Case into three separate posts - one for each driver.

We’ve already covered:

Today we cover:

LT Driver: The Fundamental Case: Coal-to-Gas Switching

What we’ve yet to cover:

LT Driver: The Fundamental Case: LNG Capacity Hitting the Gulf in 2024/25

LT Driver: The Fundamental Case: The Pivot to Electric Vehicles

LT Driver: The Political Backdrop

5 stocks to benefit from the execution of each driver

Coal-to-Gas Switching

Natural gas is being dubbed the “transition fuel” given its relative abundance, affordability, and lower emissions vs. its coal counterpart. We can see the energy mix in several countries phasing out coal in favor of natural gas to reduce emissions, lower energy costs, and improve overall quality of life.

Natural gas combusted in a power plant emits about 50% less CO2 than a coal-fired plant. This makes the coal-to-gas switch THE lowest hanging fruit when it comes to decarbonizing the grid.

The transition from coal-to-gas compared to coal-to-renewables is:

Inexpensive

minimal new power lines needed to construct

cheaper than a greenfield renewables project

Easier

land procurement is no issue since they often take up the land of the retiring coal plant

the transition to renewable energy requires the *perfect* plot of land – close proximity to substations, abundant solar/wind energy to capture etc.

Safer

Natural gas is a reliable source of energy

Renewables are intermittent and can cause serious issues, such as blackouts, when renewable penetration in a grid crosses 50-60%

Removing 50% of carbon emissions from coal combustion would make the largest dent in global CO2 emission reduction history. Coal makes up 22% of electricity demand in the U.S., but half of coal plants in operation have already announced retirement dates.

With renewables highly unlikely to fill in the gap, natural gas is likely to shoulder the weight of the transition.

Let’s run this napkin math on a global scale.

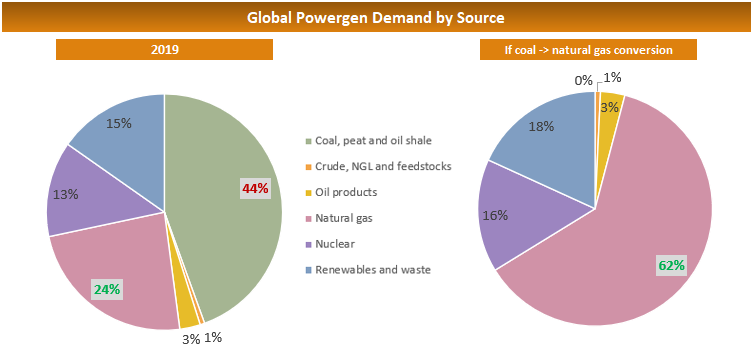

In a hypothetical scenario, what would the replacement of all the world’s coal-fired generation plants for natural gas look like in terms of natural gas demand and CO2 emissions impact? So coal -> natural gas = xx more gas demand and yy less emissions.

Demand Impact

According to the IEA, total global coal demand from the power-generation sector was about 103.6 exajoules in 2019. BUT. The average coal-fired plant has an efficiency of about 37%. So the total useful energy coming from coal is actually 38.3 EJ.

Now, let’s assume the energy equivalent is replaced by natural gas. 38.3 EJ.

We should first adjust for the average efficiency of natural gas fired plants, which is about 58%. That would get us to total gas supplies of 63.1 EJ. Meaning, that’s how much additional gas demand there would be if we replaced all coal-fired plants with natural gas.

In more relatable units,

this would translate to an additional 172 bcf/d of global gas demand for the power generation sector.

To put into context, total gas demand today sits at around 463 bcf/d.

A 37% increase would undoubtedly dub this shifting energy regime as a “transformation” rather than a “transition,” even if just a portion of that actually came to fruition!

Emissions Impact

Now we run the same napkin math on CO2 emissions. According to the IEA, coal-fired plants accounts for 30% of total CO2 emissions. About 10 gigatonnes in 2021.

If natural gas power plants emit 50% less CO2 (IPCC), replacing all coal plants in favor of natural gas would reduce global emissions by 5 gigatonnes!

Even more if accounting for the difference in power plant efficiencies!

To put in context, total CO2 emissions in 2019 was 36.3 gigatonnes. 10 of that from coal-fired power plants alone!

If we reduced this by 5 gigatonnes,

global CO2 emissions would fall by 20%!

This is by far the lowest hanging fruit in terms of decarbonization.

Though this would push back the timeline to achieve Net Zero by 2050, it’s CERTAINLY the most responsible path to undergoing an energy transformation.

This is the largest demand driver of them all, in our opinion. Of course we won’t replace 100% of coal fired plants with natural gas - even just a small portion however would still result in an enormous impact on the gas markets. It’ll call on demand where supply hasn’t even spring up. This will underpin our thesis behind long-term investing in Permian Gas Infrastructure names such as TRGP, EPD, ET, LNG, KMI, WMB, etc.

In the next series we’ll look into The Pivot to Electric Vehicles and do some more napkin math quantifying the impact its growth will have on the grid. More grid demand = more generation demand.

But all from renewables..?

Until next time!

Disclaimer: None of this is deemed to be financial advice. The author is a holder of some of the stocks mentioned in this article. Invest responsibly and with personal conviction.