Putin's Price Hike: Fact or Fiction?

Putin's Price Hike: Fact or Fiction?

A Post-Mortem and Outlook for Oil and Gas Prices

Today we take a break from our Permian Gas Infrastructure Installment - a series of several drivers underpinning our bullish thesis on gas midstream infrastructure companies in the U.S – to analyze the price impact on oil and gas prices from Russia’s invasion of Ukraine.

In the midst of the energy crisis chaos, countless soundbites misled many into misunderstanding the state of the sector pre-invasion and instead attribute all price changes to the acts of Putin following the February 24, 2022 invasion of Ukraine.

Is the Putin Price Hike a way to simplify the impacts of elevated prices we see today?

Does it carry some truth?

Or does it take advantage of a shocking event to advance a narrative in-line with political interests?

The answers are of course nuanced. But the key takeaway is that the price increases leading up to the invasion *vastly dwarfs* the impact of prices post-invasion.

Today we analyze oil and gas prices leading up to the invasion, the change of flows and legislation made post-invasion, and a brief outlook on where we see prices headed.

Putin’s Price Hike: Political Spin or Hint of Truth?

Like anything involving politics, sound bites are often misleading and do a great job masking the nuance behind a complex situation.

Does nuance matter? We would argue yes – *especially* when discussing the sensitive, long-cycle commodity market.

Let’s get nuanced.

The escalation of the war in Ukraine really began in 2014 when Russia’s military annexed the Crimean Peninsula (or 2013 when Ukraine protests first erupted).

For the purpose of this post we’ll focus on the most recent escalation and when it exactly began.

Finding this point in time is crucial to tracking changes in price. We can see very clearly how much of a commodity’s price movement was a result of the invasion vs. how much was already baked in.

We’ve identified 2 crucial dates for this discussion and analysis:

December 17, 2021

first recent escalation when Russia demanded NATO pull back troops and weapons from Eastern Europe and bar Ukraine from ever joining

February 24, 2022

Russia attacks Ukraine

just 2 days after Germany officially axes plans to turn on Nordstream 2

after many countries began enacting strict sanctions on Russia individuals and businesses

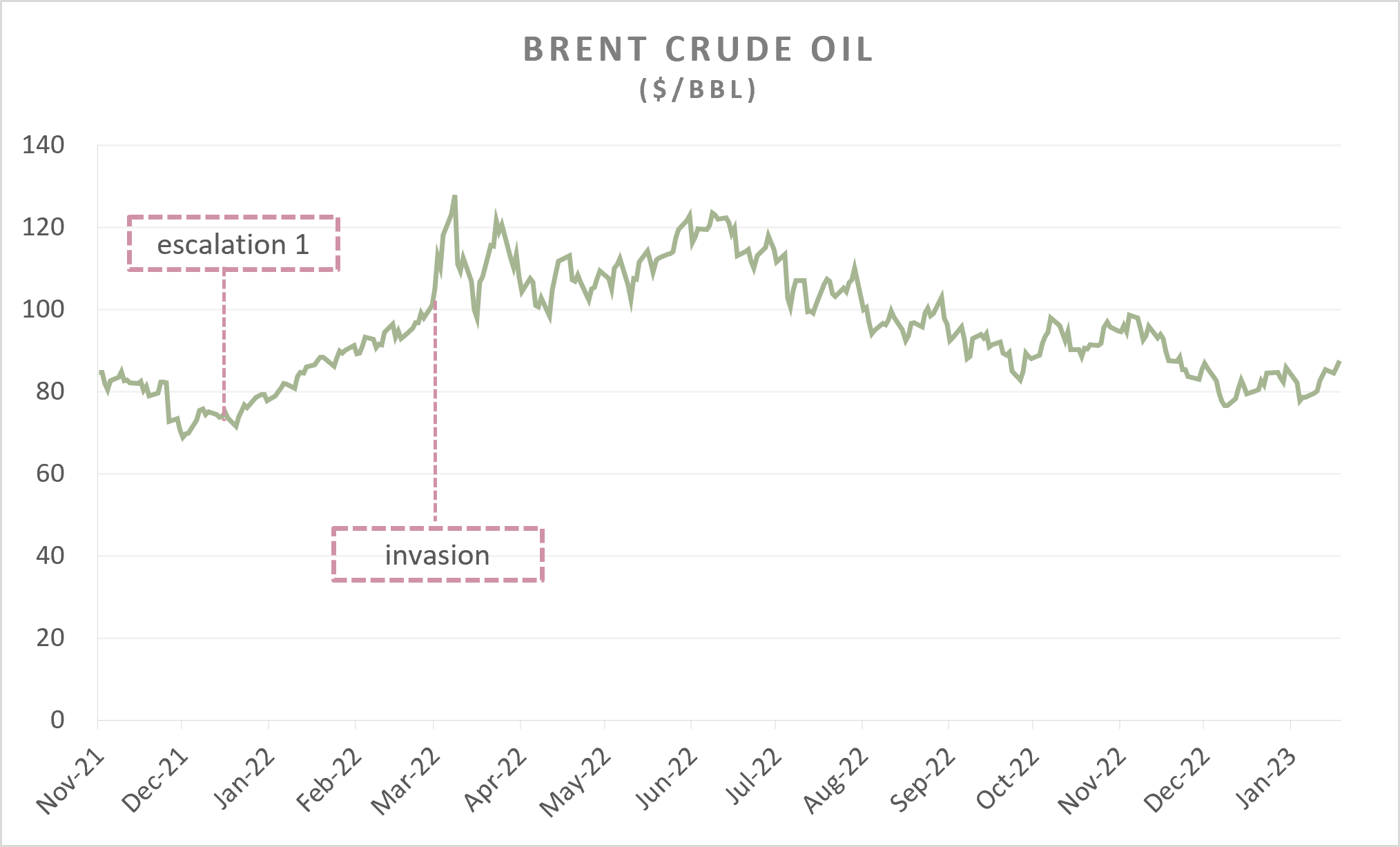

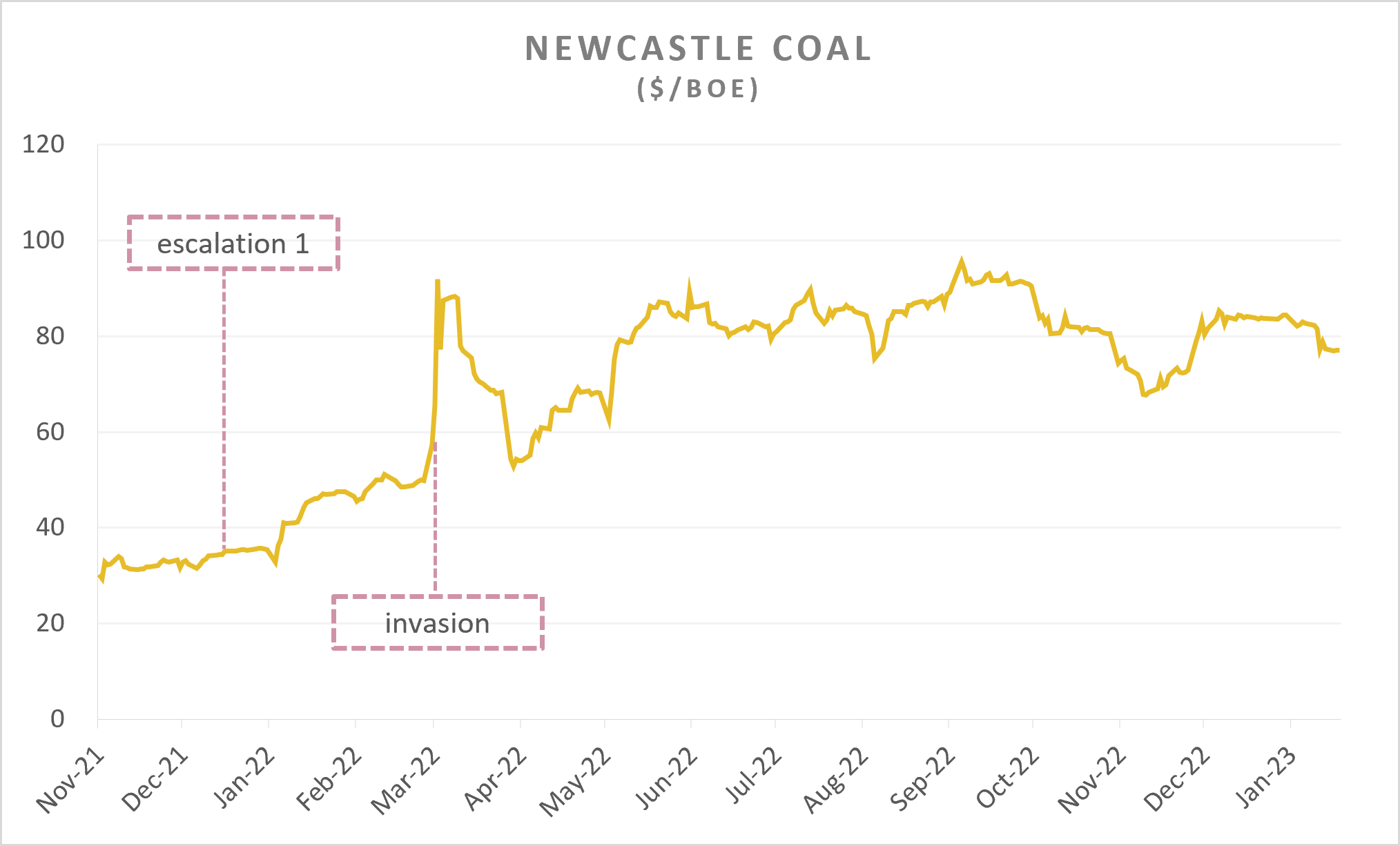

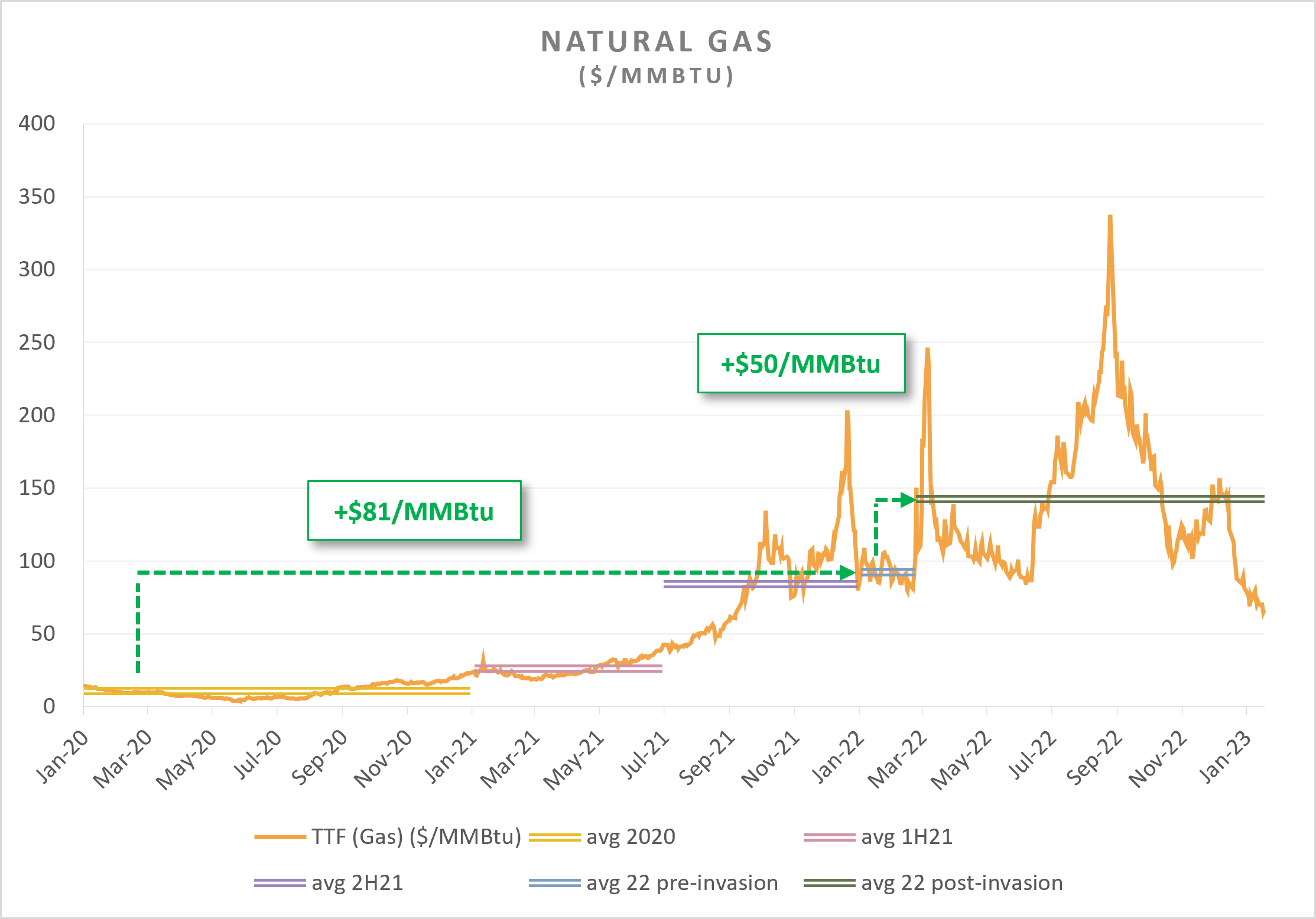

We can see the most impactful commodity price spike around these two dates. We start with gas here, given it’s the most sensitive to the situation at hand.

The crude price reaction was muted at the first escalation, but fear gripped the market following reports of the Russia invasion.

And the same goes for coal…

We can see that there clearly was an impact to all 3 primary energy prices, which make up 82% of the world’s energy consumption, as a result of Putin’s actions.

But how does it compare vs. the historic run-up prior to the invasion?

Let’s go through each in some detail, with the main focus on gas, to see whether Putin’s Price Hike is a bunch of malarkey.

Unprecedented Natural Gas Price Action

Natural gas was the commodity most directly and severely affected by Russia’s invasion of Ukraine.

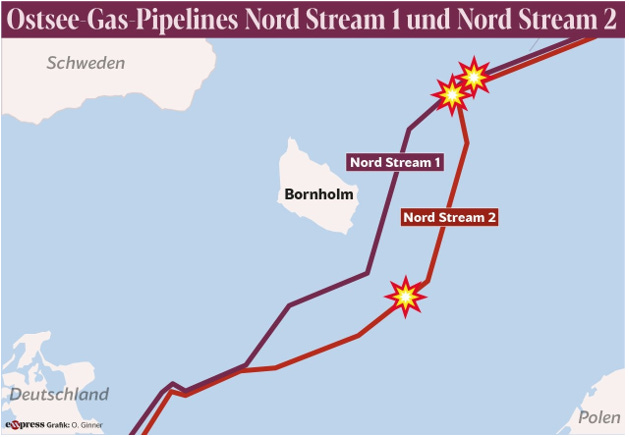

So much happened in late 2021 and 2022 on the natural gas front that we forget just how damn close Nordsteam 2 was to flowing gas.

The monstrous $11 billion pipe was fully built out - relevant connections have been made and was simply awaiting the green flag from Germany’s regulators.

They were so close to approving flows too.

The appealing pipeline came at *just* the right time – in the midst of 2 brutal natural gas price spikes due to global supply shortages and demand squeeze.

It was like waving a tuna sandwich in front of a black bear that’s fallen behind on their hibernation binge.

It would’ve have put a nail in the coffin for any potential dream of achieving energy independence in Europe. NS2 sure would’ve come in handy as Europe was battling with a tough gas situation.

Gas prices were significantly elevated before the Russian invasion of Ukraine. Did the prior fundamental supply and demand factors outweigh the impact of Putin’s invasion on natural gas prices?

Let’s take a look.

Price increase before the invasion: +$81/MMBtu

Price increase “as a result of” the invasion: +$50/MMBtu

Percentage of the price increase we can attribute to Putin: 38%

Lets take a moment to realize how INSANE these prices are. To put into context, US gas prices haven’t hovered over $10/MMBtu since 2008! Imagine receiving a utility bill > 10x what you currently pay? (And could we expect this in the future?)

Long-time readers of The Energy Transformation know exactly why gas made such a sharp, dramatic run-up from 2020. We won’t rehash it here, but you can check out the bullet points here.

In case it isn’t clear, not all of the price action post-invasion is necessarily attributable to Putin’s actions. Price declines were aided by warmer-than-expected weather and demand reduction plans from the EU. In the same tune, price increases were aided by higher demand from Asia, which helped push prices to all-time highs.

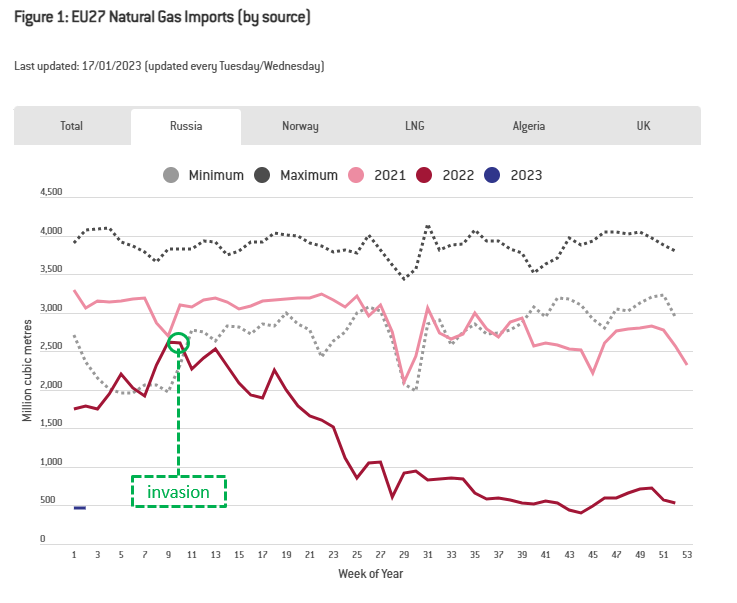

Regardless, the main culprit of the natural gas elevation post-invasion, by far, was the reduction of gas flows into Europe - going from supplying 40% of the EU’s gas needs to ~10%.

Then the sabotage occurred.

Who exactly was behind it remains an astounding mystery. The sabotager of BOTH NS1 and NS2 is to thank for the historic gas crunch Europe will face in the coming winter of ’23-24.

Prior to the sabotage, NS1 was halted anyways, but the allegedly irreparable pipelines now have very slim chances of re-entering service, no matter how bad things could get.

Conclusion: Putin certainly dealt a heavy blow in driving European gas prices higher (he cut over 1/3 of the EU’s gas needs in just one year!). It was his actions that helped drive gas prices to record highs - for a brief period. Despite all this, the fundamental factors that drove gas prices higher since 2020 had a MUCH (62%) greater impact than Putin’s invasion did.

Putin’s Price Hike? SPIN.

The Crude Price Spike

The initial price action in crude following the invasion was simply traders baking in geopolitical risk premia.

Of course, there were many threats and sanctions enacted by oil-hungry nations to cut off Russia’s most prominent revenue stream that followed:

March 8, 2022

The US banned imports of Russian oil, gas etc. (which didn’t do much - <2% of US crude supplies came from Russia)

April 6, 2022

UK pledges to do the same by the end of 2022

June 3, 2022

The EU adopts a plan to selectively prohibit energy flows from Russia

December 2, 2022

G7 nations agree on a $60/bbl Russian oil price cap – meaning, these nations can only purchase Russian crude at a price of $60/bbl or less

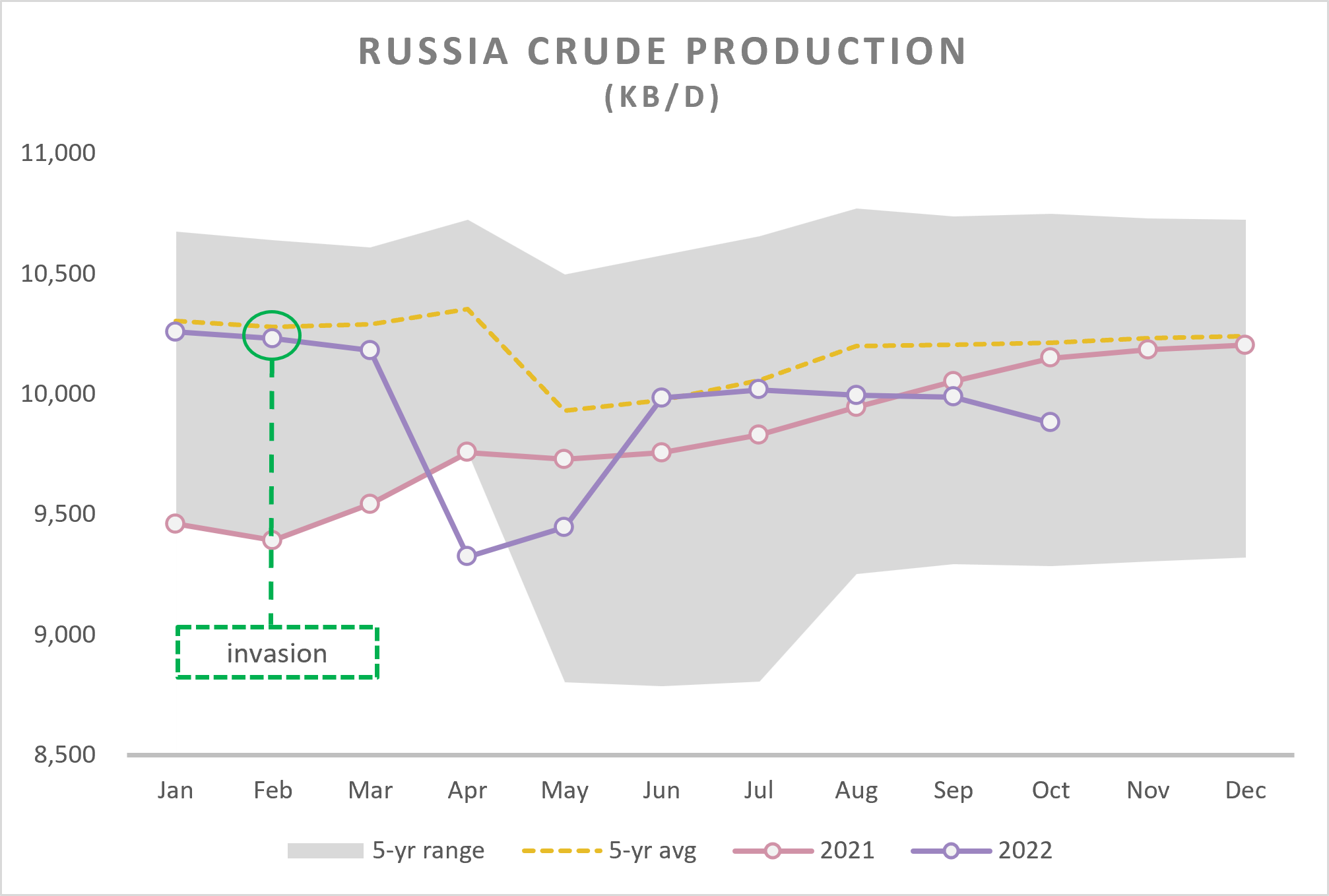

In hindsight, despite nations’ efforts (some sincere, some superficial) to cripple Russia’s prized oil sector, Russia STILL produced crude around its 5-year average.

Some things that skirted nation’s efforts to cripple the Russian oil sector: ghost vessels, Russia mixing crude with other grades at foreign ports, bans on Russian crude by nations whose Russian imports are slim to none, countries like India not abiding by the global ban or price cap, etc.

Back to the price action

The crude price action wasn’t really a direct function of Putin’s invasion, it was moreso the decisions OTHER nations took that impacted prices.

This is unlike the natural gas story, where Putin had a direct hand in halting gas flows by playing Nordstream games.

Price increase before the invasion: +$46/bbl

Price increase “as a result of” the invasion: +$11/bbl

Price increase we can attribute to Putin: 19%

Its much clearer here that the fundamental factors leading up to the invasion had an outsized impact on the price of crude, 80% more than the impact from the invasion (and nation’s efforts to cripple Russia oil industry) itself.

The “Putin’s Price Hike” really came about when addressing elevated gasoline prices in the US.

Conclusion: Gasoline prices closely track crude. To say high gasoline prices was a result of Putin’s invasion is therefore purely political spin. Putin had hardly any hand in manipulating crude oil prices. Initial volatility was largely a function of traders anticipating higher-for-longer geopolitical risk premia.

Fundamental energy supply and demand issues that caused the historic run-up from $43/bbl in 2020 to $89/bbl pre-invasion are what need to be addressed.

Not deflected.

Wrapping Up

Putin’s price hike is, for the most part, a bunch of malarkey.

He certainly played a direct hand in driving historic European gas prices higher, which had a knock-on effect on the rest of global industrial input costs (see: ammonia/food prices, steel costs etc.).

But as we’ve seen here, the majority of the energy price increases (62% for gas, 89% for crude) were a result of fundamental issues such as:

Investment in renewable capacity nowhere near outpacing reduction in global oil and gas supplies

Legislation demonizing reliable energy supply sources

Investors demanding capital discipline for multiple reasons

An unexpected and drastic rebound in Asian industrial demand

etc.

Bonus: Brief Oil and Gas Price Outlook

We have high conviction in the path gas prices are likely to take over the next 10 years. In fact, several of our most recent posts have all been directed towards the opportunities we see in the sector in the short, medium, and long term.

The gas price path will vary drastically depending on location.

US gas prices will remain relatively depressed until 2025 or so, when it will close the gap with international prices as LNG capacity swarms the Gulf Coast.

European gas prices will see increased volatility leading up to the winter of ’23-24, but will likely be the last year we experience global natural gas volatility – barring other geopolitical or legislative events.

We have less conviction in our oil price outlook given its ease of manipulation by OPEC and its relative demand elasticity compared to gas in the event of a recession.

We do expect a relative oil price floor of about $65/bbl.

One primary reason being the refilling of the now-depleted Strategic Petroleum Reserves, which will be a significant source of incremental demand highly likely to move markets.

Another reason for crude likely to hover over $65/bbl is the drastic declines and lower profitability shale producers will face.

Continued pressures on new supply will underpin higher oil prices in the long-run.