Global Energy Crisis - Part I

How we got here - narratives vs. facts

There’s no shortage of narratives regarding today’s global energy landscape (October 31, 2021). Specifically as it relates to securing energy supplies, various actors with different vested interests are quick to blame anemic energy supplies on just one or two causes. In reality, it’s the culmination of many factors resulting in a “perfect storm” that’s causing fossil fuel prices to go parabolic, which the world still relies so heavily on. Fossil fuels made up 83% of global energy consumption in 2020.

The immediate impact of today’s crisis:

higher energy prices will be passed on to consumers and businesses in the form of: higher prices for electricity, heating, gasoline, ammonia, petrochemicals etc.

The medium (long?) term:

shortages and price increases in key industries as production is dialed back for: fertilizer (food production), steel and cement (infrastructure), plastics (everyday consumer goods)

The long term:

policymakers and various actors ramping the rhetoric on the direction the world should take to ensure secure energy supplies in the future. The direction that will take place, however, is tough to know at the moment

the heroic narrative will always prevail, whatever that may be, as decisions in the long-run are always made by the constituents of a civilization

Natural Gas Shortage

The world’s suffering from a natural gas shortage. The fuel is important for heating homes during the winter and producing ammonia, which is needed to make fertilizer needed to plant crops and feed the population. You can see there’s a fundamental scarcity of the resource given how long elevated prices have sustained.

Nations need to secure sufficient fuel supplies ahead of winter to make sure they can fulfill demand (winter heating consumes MUCH more gas than summer cooling). The struggle to secure sufficient supplies led to:

competitive bidding wars on gas (LNG) cargos between Asia and Europe

firing up coal and oil plants

nations opening up to a NordStream 2 deal

shutting down key industrial facilities all in an effort to save fuel needed for the winter in residential homes.

If it proves to be a cold winter, energy prices will move higher. So far October has shown to be a slightly warmer-than-average winter, but a lot of uncertainty remains about November and beyond.

A cold winter would have drastic knock-on effects for energy, food, and other commodity prices that will disproportionately impact the middle and lower class.

How did we get here?

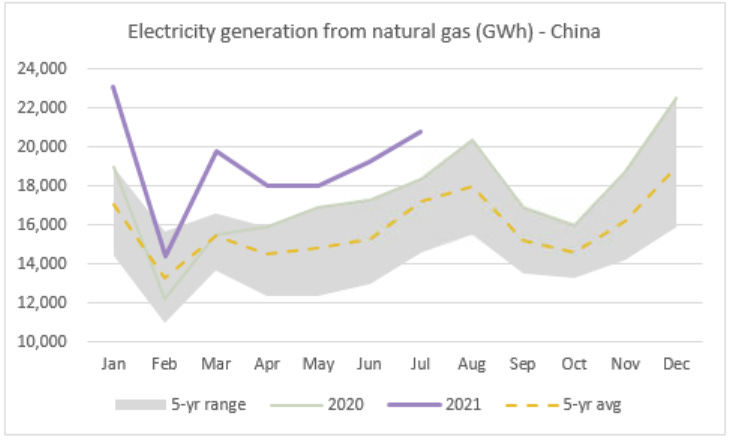

1. Elevated Asia Demand

A hotter-than-normal summer led to Asian countries bidding on liquefied natural gas (LNG) cargos to support increased cooling demand.

The incredible pace of demand recovery following months of COVID restrictions was also a surprise, particularly in China - so more fuel was needed to support industrial demand (steel-making, chemicals production, ammonia production, refinery etc.)

2. EU recovering from last winter

Remember how cold it was last winter? The Texas Freeze? Well this weather was global and led to Europe’s natural gas supplies depleted by March 2021. They began ramping purchases of LNG (gas) in the spring and summer to try and replenish those inventories and be prepared for this winter.

Unfortunately, given increased demand from Asia during that summer, Europe wasn’t to fill inventories at a comfortable level for this winter. Bidding wars between the two nations ensued, and global gas prices began to rise.

Usually at this time of year (late-October) the EU would have over 90% of its storage capacity full of natural gas, with 20-30% remaining by end of winter (nice cushion). So 60-70% of their inventories get depleted during the winter.

Today, EU inventories are at a mere 77%. If it’s a cold winter, its possible to see this drop to below 10% by winter-end, which would be disastrous.

3. Russia restricting gas flows to EU

The EU imports about 40% of its gas from Russia. Despite their increased demand for the fuel this past year, less gas actually flowed through Russia pipes to Europe. There are various reasons being cited for this. Russia claims they had their own demand to take care of, which reduced flows to EU. Many believe the move to restrict flows to Europe was done to leverage NordStream 2 pipeline approval, which would substantially increase gas flows to Europe. However it’s unlikely to meaningfully contribute to replenishing Europe’s gas inventories until the end of winter.

4. Hurricanes disrupt Gulf Coast production

Hurricane Ida hit the Gulf Coast in September 2021 and resulted in 1.1 bcf/d of gas production being shut-in throughout the month (about 1% of US production). This was the highest in history behind Hurricanes Gustav/Ike in 2008 and Katrina in 2005.

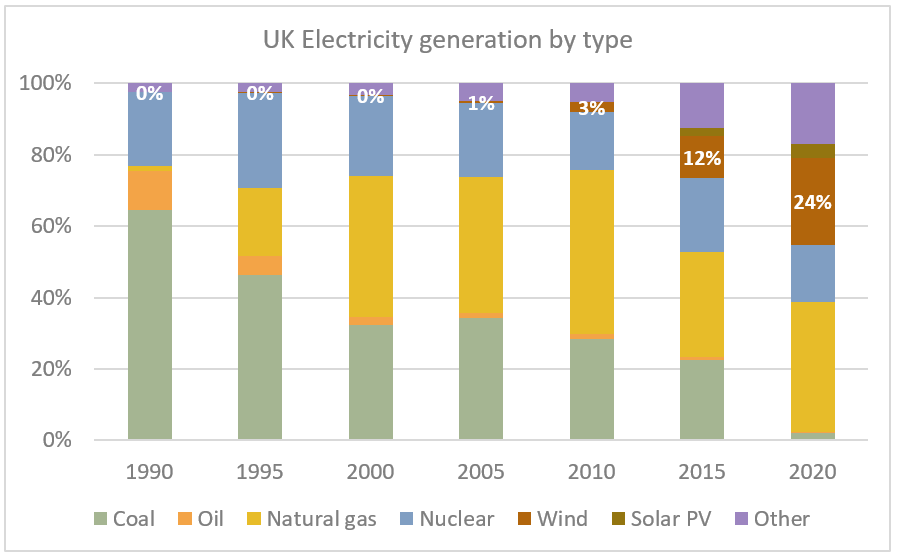

5. Low wind power generation in the UK

In 2020 wind power generated over 24% of the UK’s electricity, a significant portion of its grid. When the wind was not as strong as forecasts said for 2021, the UK sought other energy sources to fill the gap.

The UK was going to shut down their last coal plant by the end of 2022, expected to be a historic event ever since the first coal plant in the world was constructed in the UK over 300 years ago that kicked off the Industrial Revolution. The latest shortage of energy put a wrench in these plans, forcing them to bring online an additional 1-2 coal plants and delaying plans of shutting down its last coal plant.

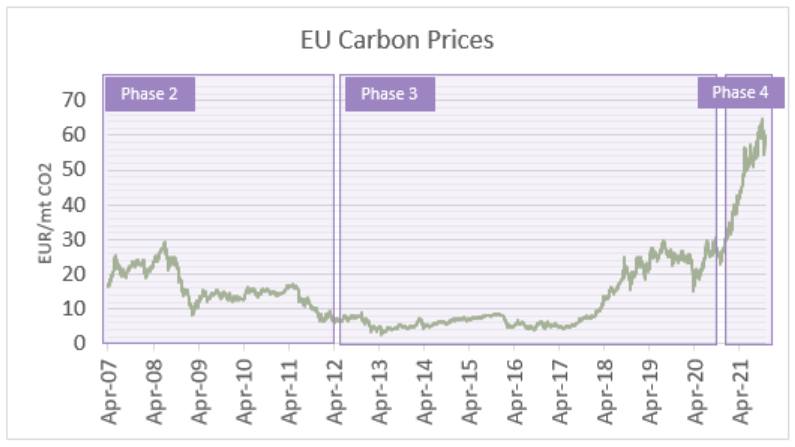

6. All-time high Europe carbon prices

Europe implemented Phase 4 of its Emissions Trading Scheme in January 2021, which significantly lowered the amount of CO2 companies were allowed to emit. This means if they went over their CO2 emssion allowance, they had to buy carbon credits in the open market. Well you can see by this price chart that many had to load up on allowances since they cannot lower emissions as fast as the EU was regulating. This led to carbon prices skyrocketing.

The unintended consequence was that coal plants began to turn off, shifting the burden onto lower-emitting natural gas power plants. This further exacerbated the global natural gas shortage.

7. Under-investment in reliable energy sources

Regulatory hurdles prevented the Appalachia region from building out natural gas pipelines, so although they COULD produce more gas, lack of transportation capacity prevents them from doing so. The Appalachia region is one of the most prolific natural gas producing regions in the world.

Global commentary around the push towards net zero pushed financial institutions to reallocate capital to clean energy companies. This increased oil and gas companies' cost of capital and deterred them from further investing in production growth (along with shareholder pressure).

LNG infrastructure was not built at the pace developers sought originally. They can only go forward on a project if they have 20-year commitments from buyers (foreign utility companies mainly). But these utilities are reluctant to enter such long-term agreements for fear of getting hit with a carbon tax that would drastically impact returns. A lot of projects were deferred and even cancelled as a result.

Though investment increased for renewable energy resources, it was not enough to cover the increasing energy demand of the world. Without ample investment in traditional energy sources to help fill the gap, we are left with a severe shortage that will have long-lasting implications on the way policymakers think about their nations’ energy security.

As you see, the blame can’t really be pinned on any one cause, though many will attempt to justify that some one cause was the main driver of the energy shortage.

In the next part of this series we’ll look at what it would take to avoid a full-blown energy crisis this winter. We’ll also go into some detail on the longer-term implications of an energy shortage in today’s context.