Gas Infrastructure Opportunities in the Permian

Series Installment: Identifying 2nd Order Plays in the Current Energy Regime

Oil go up – buy oil producers.. Right?

Simple. But many are beginning to believe this to be a crowded trade, particularly the U.S. shale producers traded on the liquid NYSE.

Inflationary pressures on capex, depleted Tier 1 inventories, decline rates catching up to their bottom line, and political risk are all reasons to be weary of another monster move to the upside amongst shale producers.

Anecdotal signs reminiscent of prior cycle-highs are also re-emerging (see: Harold Hamm’s big decision in 2022 and 2014, share buybacks despite promises to conduct them during cyclical lows, etc.)

Some will cite energy’s historically low makeup in the S&P as a reason to believe the bull run is only getting started. Though it has its merits, on its own it is NOT a driver for the U.S. oil space. We won’t rehash the argument here, but check out the following thread to see how this is potentially misleading as a driver:

Reasonable catalysts for further upward momentum amongst oil producers globally will be:

Institutional flows ditching ESG mandates, resulting in higher multiples

Major indices re-shuffling sectors to weigh more towards energy companies

Crude continues to climb amid continued underinvestment and misguided policy

Crude strip reprices upwards across all months (December ‘23 contract trading at $80 WTI)

Most of these catalysts are not only reasonable but likely to occur and result in the continued outperformance in oil producing stocks.

HOWEVER - those with experience in the markets know that real alpha lies in the companies impacted to the 2nd and 3rd derivative. Areas where the trade has yet to catch up. The risk-reward is positively skewed towards these players.

If you’re interested in knowing who these players are and the countless long-term drivers supporting the trade, I suggest reading on.

The Gas Infrastructure Trade

In this series, we will look at gas infrastructure. Names that will benefit from a multitude of catalysts on ALL time frames. The downside potential is understood, though the upside case is vastly overwhelming.

What we’ll cover in this series:

Top-Down Framework of the gas infrastructure trade (here)

ST/MT Driver: The Event-Driven Trade

LT Driver: The Fundamental Case

LT Driver: The Political Backdrop

Deep Dives into a handful of stocks that’d benefit from the execution of each driver

Why Gas Infrastructure?

The names we will go over are primarily structured as “toll-road” businesses. They get paid based on volume flowing through their systems (pipeline, LNG plants, processing plants, frac facilities etc). Most have secured “take-or-pay” contracts – meaning the midstream company gets paid regardless of whether its customer decides to push product through its systems.

A high % of take-or-pay contracts vs. other contract structures makes a stock more stable over the long-term, especially if secured with reliable counterparties. That’s why the names we will cover won’t have as much torque as say a $100 million market cap shitco which could moon or go to zero in the blink of an OPEC eye. BUT. They make great candidates for anyone’s long-term portfolio. Rock-solid holds especially given:

Today we’ll lay out a brief summary for each of those drivers.

Over the coming weeks we will dive deep into each and use those frameworks to underpin our conviction in the bull case for U.S. gas infrastructure companies. Much of these drivers have significant overlap with other areas across the value chain, but the focus will be on gas infra for now.

After we flesh out the framework for each of these drivers (and their potential drawbacks) to aid our personal conviction, we’ll then conduct deep dives on various companies that will benefit from the frameworks we’ve laid out.

1. The Event-Driven Trade

The oil-driven Permian basin continues to grow in activity levels, though not as fast as it once has. The average well’s age is rising – and overtime, shale wells tend to produce more gas as a % of the total hydrocarbon stream

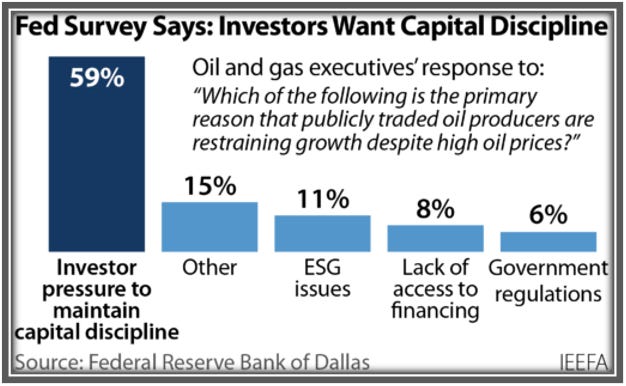

So although oil production in the basin is rising, gas is rising even faster as publicly-traded producers practice capital discipline in the face of investor demands, among other (highly-debated) reasons

The rapid expansion of gas production is outpacing the basin’s infrastructure capabilities, which will lead to severe bottlenecks. Producers will have no alternative takeaway options as they did in 2018 when this problem occurred, where it was more socially acceptable to flare excess gas.

This will have severe knock-on effects for both oil producers and infrastructure providers mainly in the form of widening Waha-Henry Hub differentials

2. The Fundamental Case

A slew of LNG capacity is set to hit the Gulf Coast starting late-24/2025 – exporters will need all the gas they can get to ensure molecules make their way to their respective counterparties

Incremental gas flow won’t be coming from the blessed shales of the NorthEast - which have been cursed with political barriers entirely preventing gas pipeline infrastructure

Haynesville will help, no doubt about it – but the Permian will have an equally burdensome role to play in providing the world with abundant and cheap hydrocarbons

The inelasticity of natural gas demand builds an inherent floor on the level of global consumption

Longer-term electricity demand is only set to rise as:

Coal, oil, biomass and other higher-carbon fired power plants are retired

The pivot from Internal Combustion Engine Vehicles to Electric Vehicles calls on increased grid electricity flows

Developing nations can’t afford the high up-front costs of establishing renewable + battery-based electricity solutions

3. The Political Backdrop

There’s a lot of overlap in this one with the fundamental case, event-driven trade, and doomsday scenario – but we’ll separate this section out to focus on it specifically

Tougher to get infrastructure built = higher value for infrastructure already built

The Biden Administration has cancelled the Keystone XL pipeline, which could have supplied the U.S. with much needed heavy crude

Infrastructure permits - particularly in the abundantly energy-bestowed North East - is becoming increasingly difficult and in many cases even impossible to construct pipelines, creating gaps unable to be filled through free markets

Dutch courts mandates Shell reduce the CO2 emissions of its activities by 45% at the end of 2030 compared to 2019

The Net Zero narrative charges on – and the answer is “no more fossil fuels,” despite energy demand expected to more than outpace wind and solar installations

These are the 3 primary drivers across all time frames for the gas infrastructure sector. We decided against the inclusion of a Doomsday Scenario for two reasons:

It has the potential to take on many forms, especially if getting into potential war dynamics. It would reach a point where an analysis would be nothing more than imaginative

In each of the 3 drivers outlined above, taking any of its sub-drivers to an extreme could pass as a “doomsday” scenario

Company Deep Dives

We will tie in the drivers discussed above with the best vehicles that would benefit from them.

Feel free to ask about any of the metrics or a specific company in the comments below!

Here’s a brief summary of the companies and content we’ll cover in our company deep dives:

Heads up: Names like EPD 0.00%↑ and ET 0.00%↑ may appear to be relatively undervalued on a multiples basis, but the main reason is because they operate as MLPs instead of Corporations.

Institutions (and retail) often don't want to bother with the Schedule K-1 tax form that comes with ownership of an MLP, and therefore look for other vehicles to gain exposure.

Note: Values are shown as of 11/07/2022

The Deep Dives will go into the types of assets each company operates, the progression and state of their cash flows and balance sheet, current and future returns to shareholders, exposure to various industry themes etc.

Perhaps we also do a special deep dive into a super high risk gas infrastructure co. with a ton of stock-torque + meme-stock potential

The gas infrastructure sector in the U.S. is undoubtedly positioned well to take advantage of the numerous coming catalysts which span across the entire timeline. Some will benefit more than others given based on their structure and exposure. Although these are mainly large-cap stocks, meaning is unlikely to have the torque of a smaller-cap company, they could make for great buy-and-hold for those with the appetite and respective risk tolerance.

Disclaimer: None of this is deemed to be financial advice. The author is a holder of some of the stocks mentioned in this article. Invest responsibly and with personal conviction.