Parex Resources (PXT): An Undervalued Cash Flowing Machine

Imagine buying a shale co. instead of this little gem?

Today we take a break from higher-level industry trend research and extrapolation to take a look at an opportunity that’ll outperform peers in a rising or even stable oil price environment.

We’ll go through the thesis behind Parex Resources, a company overview, a deep dive into its assets and operations, avenues for growth, risks and mitigants, and finally arrive at a valuation and price target.

In the event that sentiment among the oil and gas space falters due to recessionary fears (despite a fundamentally tight market) Parex is still well-positioned to outperform the oil production sector.

Thesis

As the largest independent producer and acreage holder in Colombia, assets of the oil-heavy, unhedged, debt-free Parex Resources (TSX: $PXT - OTCQX: $PARXF) are in an optimal position to capitalize on a fundamentally tight oil market, with many opportunities for incremental upside.

The $2 billion company boasts industry-leading profitability metrics, exposure to Brent pricing, a near 100% oil cut, low declines, production growth, impressive returns to shareholders, and ample exploration opportunities.

The stock currently trades below its PDP-10 value as investors overestimate the impact of political and insurgency risk in the region. With the stock trading at multiples much below its high-decline, inventory-hungry shale peers, we think the operational prowess and significant shareholder returns justifies this for a strong buy as the best risk-adjusted play in a tighter-for-longer crude oil market.

Company Overview

High-Level

Parex is an unhedged pure play crude oil producer, with 97% of its 2022 production of 52 kboe/d coming from crude sourced from four primary basins in Colombia. Its headquarters is in Canada and listed on both the Toronto Stock Exchange and the OTC QX market.

Production is growing steadily and expected to continue doing so through 2025.

The forecast we show above excludes potential incremental upside from successful delineation of its exploration program, which will be stepped up overtime following its purchase of 4.3 million acres in December 2021 from the latest Colombia bidding round.

The purchase represents a four-fold increase vs. 2020 with Parex emerging as the top bidder for acreage during the bidding round, surpassing even the state-owned Ecopetrol EC 0.00%↑ . Furthermore, the government stated that they intend to halt anymore bid rounds.

The substantial purchase puts the company’s total net acreage owned across various prospective and producing blocks in Colombia at 5.5 million. The purchase makes up 78% of its overall acreage.

Primary Production Regions

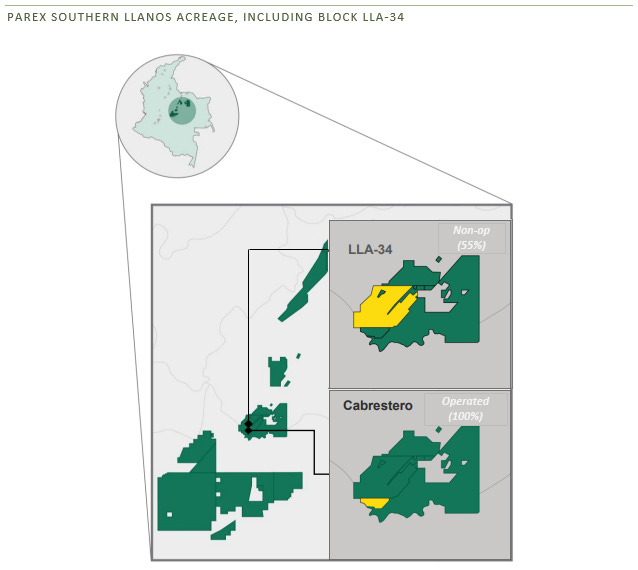

Parex operates in four primary regions; Block LLA-34, Southern Llanos, Northern Llanos, and the Magdalena Basin.

About 2/3 of Parex production came from its non-operated LLA-34 Block in 2022. This is expected to decline overtime as EOR techniques (waterflood injections) at the block indicates the region’s maturation, with capital being increasingly allocated towards operated acreage.

The LLA-34 Block is technically located in Southern Llanos, but is broken out due to its significance and its non-operated nature. Production in the block on an absolute basis is expected to remain relatively flat overtime as the operator GeoPark (45%)GPRK 0.00%↑ focuses on combatting declines through waterflood injections.

Lessons here were learned from Parex’s acreage contiguous to LLA-34 over in Cabrestero (Southern Llanos), where declines were successfully flattened and in fact, accelerated oil recovery. Over 90% of its Southern Llanos production comes from Cabrestero.

Parex generates its highest netbacks in the Northern Llanos region. Parex is 50% operator in partnership with Ecopetrol, Colombia’s government-owned integrated oil and gas company. Relatively low production in Northern Llanos (6% of total in 2022) has been a result of infrastructure restrictions, which the producer is addressing for 2023 and beyond.

Production is expected to nearly double in 2023 towards 6,000 boe/d as a result, making the basin a key growth engine. Unfortunately, the region is exposed to occasional insurgency and related instability that lead to operational shut-ins. The latest upheaval in Northern Llanos on January 2023 resulted in halting drilling operations at Araucua while shutting-in the Capachos block. Capachos was restarted 3 months later, and activity at Arauca is expected to restart in 2Q23. Its impact led to the producer guiding towards the lower-end of production guidance for 2023. A similar incident last occurred in 1H21.

Risks and Mitigants

We believe the market is mispricing Parex Resources on nearly every financial metric. The level of political and insurgency risk does not justify the current market discount. Market participants may feel a bit uneasy about a debt-free company, generating un-levered returns on its operations. However, this unique aspect reduces the company’s inherent risk and supports a floor valuation of at least the net present value of its Proved Developed Producing reserves.

Political risk is overblown. The government has demonstrated several times over its desire to keep its land open for exploitation amongst foreign companies, evidenced by allowing Parex, a Calgary-based company, be awarded the majority of the blocks in Colombia’s most recent, and potentially last, bidding round.

Sure, the government has altered its tax scheme in November 2022 to generate higher revenues from oil and gas producing companies in the country. However, the changes are nowhere near detrimental to the future growth and success for these companies. It still leaves much room for capital allocation towards exploration, development, and capital returns to shareholders in any reasonable Brent price environment.

Insurgency risks remain. Although it isn’t something we can necessarily predict, the impacts tend to be relatively muted as both the company and government actively work to mitigate any lengthy disruptions. The most recent shut-in due to regional instability led to a 90-day shut-in of one of its blocks, leading to a 4% impact on expected annual production. The prior most significant disruption occurred in 1H21, which was resolved in a timely manner. Any potential blockades or other disruptions in between have been too insignificant to report, and the company continues to deliver on its production guidance.

The overblown insurgency risk gives us the perfect opportunity to scale into the cash flowing Parex machine.

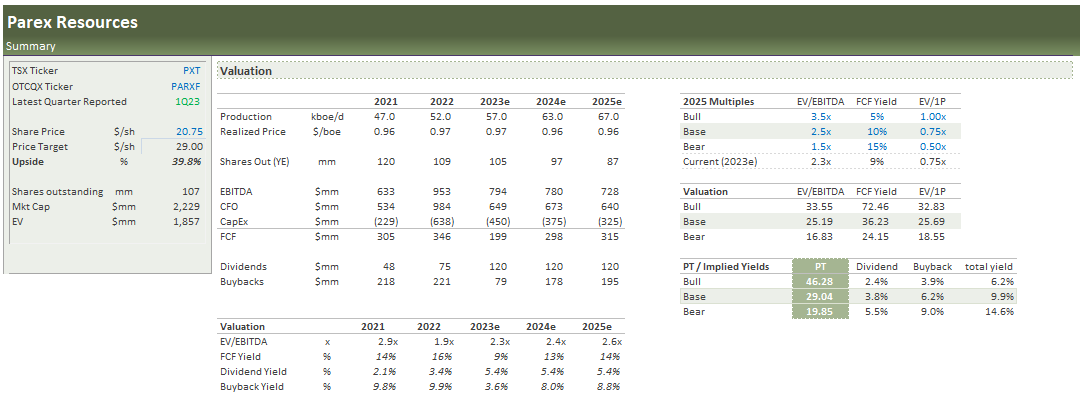

Valuation and Price Target

We arrive at a near-term valuation for $PARXF at $29/share, implying upside potential of about 40%.

The valuation is based on the average multiples of EV/EBITDA, FCF Yield, and EV/1P on a 2025e basis. This valuation uses base case multiples that are in-line with today’s market valuation, which are already weak. In other words, the multiples used to derive the price valuation are relatively conservative! They also don’t include any incremental upside from potential success of its exploration programs.

Our 2025 estimated average realized prices of $58/boe are also relatively conservative.

It’s worth noting that lower capital spending plus production growth over the next several years, particularly in this rising material and labor price environment, are practically non-existent across the shale E&P space.

These shale-based companies trade at multiples over 2x that of Colombia producers despite having a 40%+ gas cut, steep declines, depleted Tier 1 inventories, WTI exposure, infrastructure constraints, and ongoing political risk.

Our argument lies in the fact that the negative characteristics of shale companies are non-existent at Parex, which will appeal to the eyes of investors searching for growth and cash flow opportunities, which would lead to greater fund flows and fetch higher multiples.

Parex is severely discounted even in the eyes of management, evidenced by the aggressive, systematic share repurchase scheme where outstanding shares are set to decline by nearly 30% from 2021 – 2025, according to our estimates.

Production growth, declining capital spending, and increasing capital returns to shareholders has been the trilemma for the shale industry, but not Parex. Our valuation does not include upside from exploration prospects, despite accounting for it in our capex assumptions, which management is optimistic about given contiguous reservoir and production successes.

Like this post? Want access to the model itself? Want to see more/less operation vs. financial analysis, or vice versa? Let us know for next time!

Disclaimer: None of this is deemed to be financial advice. The writer owns shares in PARXF and will look to increase exposure should recessionary fears grip the market and punish oil stocks. Don’t risk more than you’re willing to lose. Invest responsibly and with personal conviction.